BLOG

800VDC, Off-Grid Power, and the Decisions That Have to Come First

July 15, 2026 · Daniel Miodovnik, COO, Andrew White, Head of Data Center Design, and Eden Smalley, Senior Mechanical Engineer, MDC

In Q1 2026, CoreWeave reported $99.4B in backlog with 3.5 GW contracted power but only 1 GW active; the issue lies in the speed or delivery of converting contracted power into energized capacity at their data center sites.

Queues are full, the grid is congested, and the traditional markets of Northern Virginia, Dallas, and Phoenix are running out of road. Serious operators are now making three decisions at once: 1) how the facility distributes power (the shift to 800 VDC architecture); 2) where that power comes from (off-grid and behind-the-meter generation), and 3) where to build at all (markets where both are still possible).

Each one of these creates the same underlying problem. These are engineering and procurement decisions that have to be made early, because transformers, switchgear, and generation equipment carry lead times of two years or more, so the order goes in before the design is fully settled. They have to be made correctly, because a facility architected around the wrong voltage, the wrong cooling assumption, or the wrong density target cannot be cheaply rearchitected once steel is up and equipment is on order. And they have to be sourced against a vendor ecosystem that is fast moving, where reference designs change between purchase order and delivery, and where the suppliers themselves are capacity-constrained. Those decisions determine whether contracted megawatts ever become operational compute.

Key Takeaways

What CoreWeave's Numbers Show

CoreWeave's Q1 2026 numbers illustrate where the buildout is stuck: $99.4B in contracted backlog against a target of more than 1.7 GW active by year-end, up from 1 GW at the end of Q1. The 2.5 GW gap between contracted and operational reflects construction timelines and power delivery delays, not a shortage of customers. U.S. data center power demand is projected by Goldman Sachs to more than double, from 31 GW in 2025 to 66 GW by 2027.

Those timelines aren't inevitable. They're a function of how facilities are engineered, how late the critical decisions are made, and how scarce the labor is. A single hyperscale campus now draws 4,000 to 5,000 workers at peak, up from around 750 in the cloud era, against a US construction shortfall Bessemer Venture Partners puts near 439,000. Stick-built campuses run full on-site construction, sequential permitting, and late power decisions in series, all competing for the same trades. That sequence takes time an AI deployment schedule doesn't have.

"Power and cooling decisions now have a prediction problem. A facility breaking ground today energizes in a few years time, and it has to be architected for the rack densities and thermal loads of the future, not the ones in this year's reference designs. The design has to hit a target that's still moving."

— Daniel Miodovnik, COO, Orbital

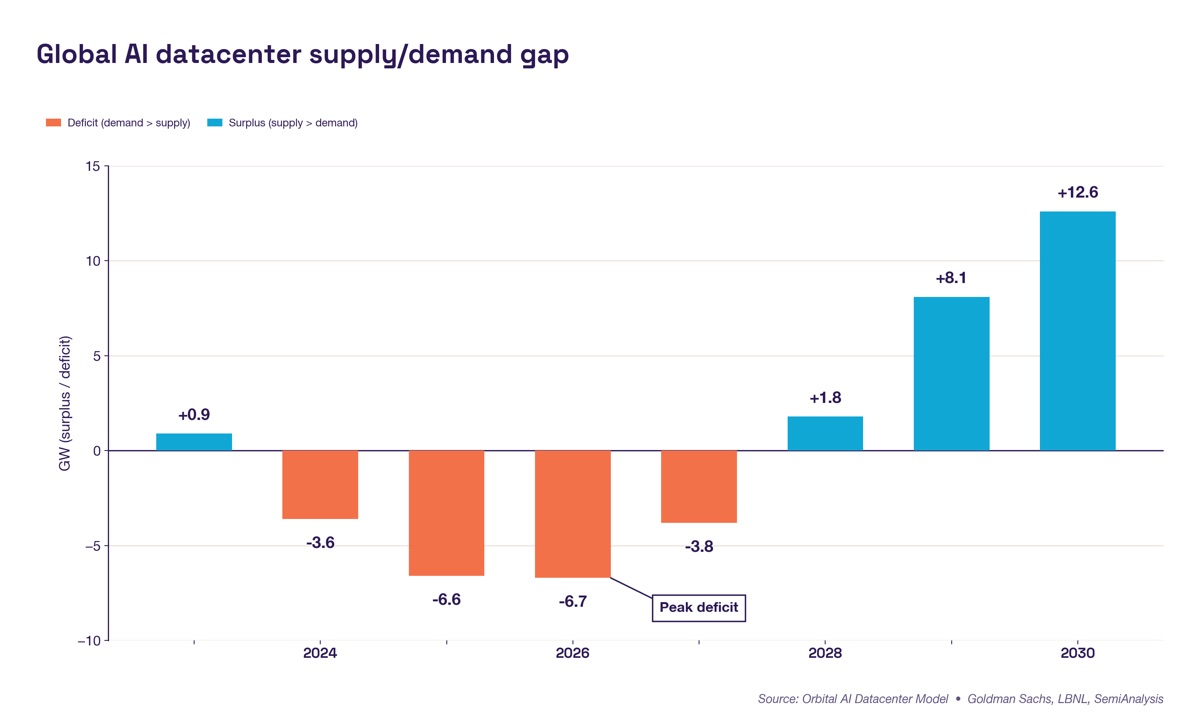

The supply-demand gap extends well beyond CoreWeave. AI datacenter capacity faces a peak deficit of 6.7 GW globally in 2026, with Microsoft and Meta each short by 1.5 GW. Source: Orbital AI Datacenter Model, estimated and extrapolated, July 2026.

What Is 800 VDC, and Why Legacy Systems Can't Keep Up

NVIDIA's 800V high-voltage direct current (HVDC) architecture delivers a 5% end-to-end efficiency gain over legacy 54V distribution, a 45% cut in copper busbar, and up to 70% lower maintenance from fewer PSU failure points. At the rack densities AI now requires (100 kW and up), those aren't marginal gains.

Legacy architecture was built for 10 to 20 kW racks, stepping utility power down through transformers to 480V AC and again to low-voltage DC at the server, losing energy at every stage. It also assumed a stable load. AI clusters don't behave that way: synchronized GPUs swing from 30% to as much as 150% in seconds, millions of load cycles a year, forcing engineers to size for the peak rather than the average. 800 VDC collapses the conversion chain so more of every watt reaches the GPU.

The industry is converging on 800 VDC. NVIDIA's 800 VDC reference design targets 660 kW, with production hardware from mid-2026, and Vertiv's aligned portfolio ships in H2 2026. The choice between 800 VDC and conventional AC distribution gets locked into the electrical design before that hardware ships, and it sets everything downstream. A facility that defaults to AC now faces a retrofit problem later.

"800 VDC isn't a component you specify, it's an architecture you design around. The busway, the protection scheme, the energy storage all follow from it, which is why it has to be the first decision, not the last. Designing for 800 VDC from a clean sheet means you aren't inheriting the conversion stages legacy infrastructure accumulated over time."

— Eden Smalley, Senior Mechanical Engineer, MDC

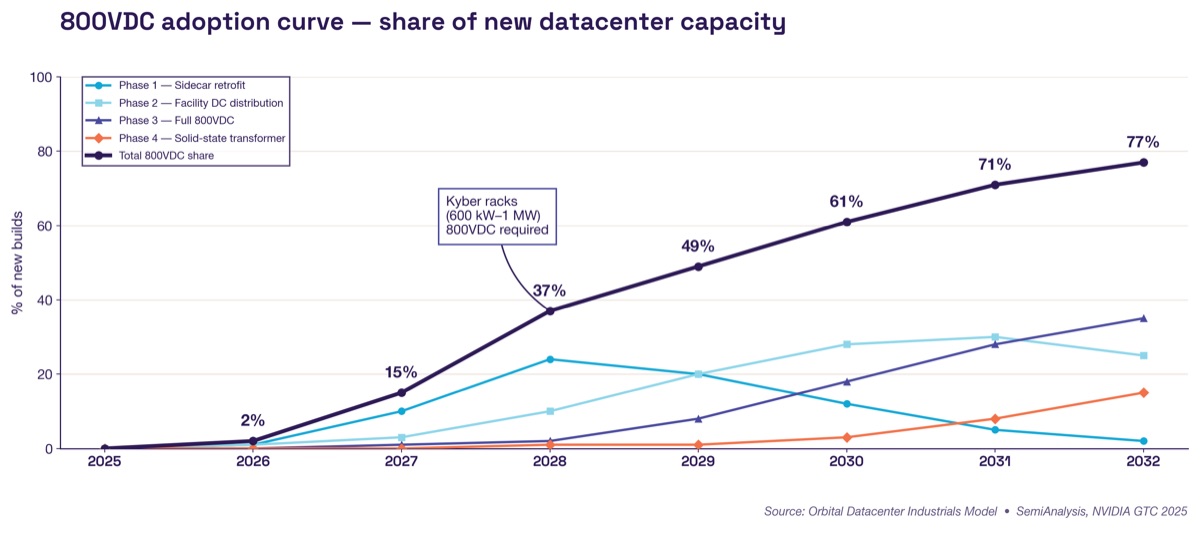

800VDC adoption is projected to reach 55% of new builds by 2030, driven in part by NVIDIA's Kyber architecture (600 kW–1 MW racks) requiring 800VDC from its newly projected 2028 release. Phase 1 sidecar retrofits bridge the transition, peaking in 2029 before facility-level DC distribution takes over. Source: Orbital Datacenter Industrials Model (derived estimates), SemiAnalysis, NVIDIA GTC 2025.

The Grid Isn't the Answer

Projects reaching commercial operation in 2025 spent an average of 55 months in the U.S. interconnection queue. At the end of 2024, more than 10,300 projects representing 1,400 GW were waiting, a backlog irrelevant to anyone on an AI timeline measured in quarters. The grid can't be the primary planning assumption.

So off-grid and behind-the-meter (BTM) procurement has moved from edge case to mainstream. Operators are contracting gas microgrids, structuring private wire deals with solar and wind, and building generation on campus. SemiAnalysis projects BTM will power well over half of new US data centers from 2028, with equipment demand crossing 50 GW a year by 2029.

The honest complication is that off-grid now has a queue of its own. Gas turbine and step-up transformer lead times have stretched to three or four years, against a historical norm near 18 months, with some developers reporting five to seven. Off-grid beats a five-year interconnection wait, but it isn't instant. At current lead times, generation is ordered first, and the compute can follow years behind it.

Getting from generation to tokens takes four steps: generate the power, connect it, convert it, compute with it. The first step is increasingly solved by the likes of LevelTen, SLB, and others who structure supply from gas to geothermal to grid PPAs. The fourth is handled by the hardware: GPUs turn watts into tokens. The gap is the two steps in the middle. Someone has to engineer the connection between whatever power the operator buys and the racks it feeds. The closer the compute sits to the generation, the simpler that engineering gets, and transmission losses disappear, because the power never travels.

"The question is no longer just the utility interconnection, it's what's available on the private side. The generation type sets the electrical interface, and the interface sets the facility design. That sequence is what makes or breaks the timeline."

— Andrew White, Head of Data Center Design, Orbital IT

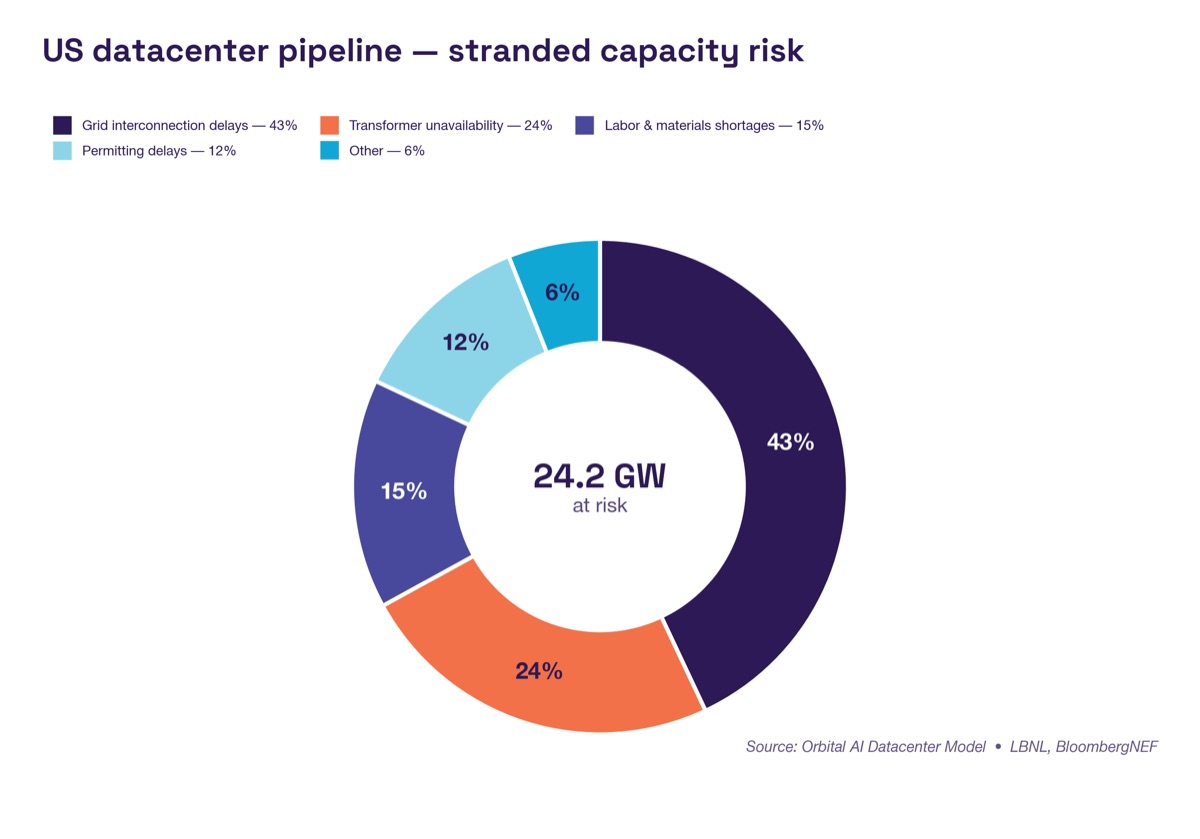

24.2 GW of planned US datacenter capacity is at risk of delay or cancellation. Grid interconnection delays account for 43% and transformer unavailability for 24% of pipeline risk. Northern Virginia faces 50% pipeline exposure. Source: Orbital AI Datacenter Model, LBNL, BloombergNEF.

Pulling the Decisions Together

Power demand is on track to more than double by 2027. The escape route from the grid is predominantly gas, where fuel comes up alongside oil faster than pipelines can carry it away and sells at a deep discount, and the strongest positions are already being claimed: Chevron is building a 2.5 GW Permian plant to feed a colocated data center, Microsoft is in exclusive talks on a $7 billion gas plant near Pecos, and Energy Transfer has signed long-term supply agreements with Oracle across three data centers.

Hardware specs, geography, and power procurement interact: the rack density sets the power architecture, the power architecture shapes what generation can serve it, and the generation determines where the facility can be. Defer any one and you constrain the other two.

The pattern is the same at every layer, and it's an engineering and procurement pattern. 800 VDC has to be designed in before the electrical backbone is fixed. Off-grid only pays if the facility is ready when the generation is: the turbine alone can take three to four years to arrive, and a facility designed serially, after the power is secured, adds its own two to three years on top. The timelines have to run in parallel, which means engineering the facility against a power source that's still being procured. This is a sequencing problem, and it's solved the same way at every layer: engineer early, procure early, and design for the conditions at energization rather than the conditions today.

Frequently Asked Questions

What is 800 VDC and why does it matter for AI data centers?

800 VDC (800-volt high-voltage direct current) delivers power to AI racks at higher voltage, eliminating conversion stages that legacy 54V systems require. NVIDIA measures a 5% end-to-end efficiency gain and 45% less copper.

Why are AI operators turning to off-grid power?

Because grid interconnection is too slow: the U.S. queue averaged 55 months to commercial operation for 2024 projects. Behind-the-meter natural gas, private wire solar, and on-site generation can cut years off that wait, provided the generation is procured early enough. SemiAnalysis projects off-grid will power over half of new US data centers from 2028.

How long are gas turbine lead times for data center power?

Three to four years for gas turbines and step-up transformers, against a historical norm near 18 months, with some developers reporting five to seven years. That closes most of the gap to a typical five-year grid queue: off-grid is faster on average, but the advantage is no longer automatic, it's earned in procurement.

Which US markets are gaining AI data center capacity in 2026?

Texas and the Midwest, projected to grow from 33% to 53% of US hyperscale operational capacity (JLL). The draw is available power, available land, and utilities with open queues, while Northern Virginia, Phoenix, and Silicon Valley face capacity, permitting, and water constraints.

What is the AI data center deployment gap?

The gap between contracted power and active power. Microsoft's demand backlog more than doubled to $625 billion in January 2026, while its CFO told analysts that demand continues to exceed available supply and guided to capacity constraints through at least mid-year. Three months later, management still described capacity as the primary limiter on Azure growth, with constraints persisting through 2026. The binding constraint is construction timelines, power delivery, and labor, not demand.